The Supreme Court’s decision rejecting IEEPA as a tariff statute is decisive on authority, but it is not self-executing on refunds. It shuts off the legal predicate for continued collection, yet it leaves a second and more operational question largely intact: how, and on what proof, will “unlawfully” collected duties be unwound across millions of entries.

The CIT’s Atmus Filtration Order Points the Way on Refunds

The Supreme Court answered the authority question. The Court of International Trade (CIT) is now answering the remedial one. In Atmus Filtration v. United States, Judge Eaton issued a refund-oriented order that reads like the first operational blueprint: CBP is directed to liquidate unliquidated IEEPA entries without the IEEPA duties and to reliquidate non final liquidations on the same basis.

Final liquidations remain the hard-edge case:

- It confirms the refund perimeter will be drawn by liquidation posture, not by broad narratives of economic incidence.

- It signals an ACE implementable relief model, likely through standardized guidance and batch processing rather than importer by importer adjudication.

- It frames Learning Resources, Inc. as a benefit for importers of record generally, reinforcing the case for uniform treatment across ports and brokers.

That order does not make refunds automatic, but it materially reduces uncertainty about which entries are most recoverable and how repayment is likely to be operationalized.

The First Distinction that Matters: Stopped Versus Refunded

Two things can be true at once:

- CBP can stop collecting quickly by deactivating IEEPA-related tariff codes and reverting entry processing to the non-IEEPA duty landscape.

- Returning money already collected is a separate exercise. In many cases, entitlement will turn on entry posture: liquidation status, timely challenges, and the remedial framework the Court of International Trade (CIT) ultimately orders.

Why The Refund Fight Will Be Entry-By-Entry

Customs law is built around the entry. Each entry has its own duty calculation, its own liquidation clock, and its own administrative posture. Even where illegality is clear, repayment is operationalized through liquidation or reliquidation, and the payment flows from a recalculated entry record.

For importers, this means the refund landscape is not a single consolidated balance sheet entry. It is a large set of heterogeneous entries across ports, brokers, and importer of record structures, many filed under urgent operational conditions and with uneven documentation.

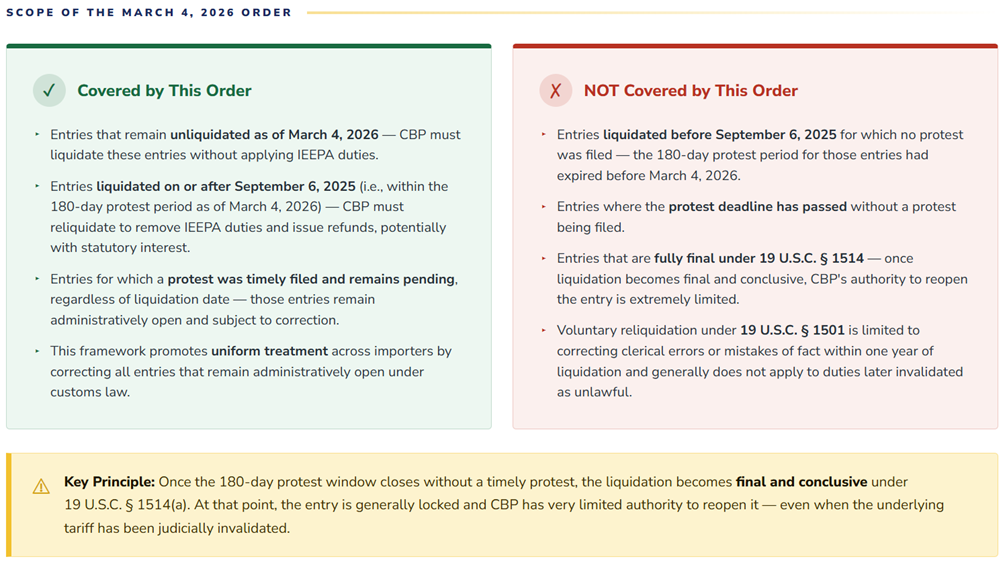

Finality Risk and the 180-Day Constraint

One structural constraint looms over any refund architecture: finality. Under 19 U.S.C. §1514, a liquidation becomes “final and conclusive upon all persons” unless a protest is filed within 180 days of liquidation. That doctrine is not procedural trivia; it is the backbone of customs administration. The government is therefore likely to argue that entries liquidated without timely protest are not automatically reopened simply because the underlying tariff authority has been invalidated. Instead, it may contend that relief is limited to unliquidated entries, entries still within the protest window, or entries covered by specific court-ordered remedial instructions.

This finality framework is the single most significant legal limiter on the scope of recoverable refunds and will shape both the breadth of any CIT remedy and the practical recoverability profile across importer portfolios. The CIT is already translating that doctrine into remedies. In the 4 March Atmus ruling, Judge Eaton directed liquidation and reliquidation only where an entry is unliquidated or where liquidation is not yet final.

Modalities of Recovery

In practice, importers should plan around four pathways, each with different friction points. After Atmus Filtration, the court-ordered track is no longer speculative; it is emerging as the organizing framework that the other pathways must fit into.

- Court-ordered relief in the consolidated CIT litigation: The most administrable outcome is a remedial framework (often shaped through test cases) that CBP can implement in ACE, with standardized claim packages thereafter. The CIT has now begun issuing refund-oriented remedial orders that preview that framework. In Atmus Filtration, Judge Eaton directed CBP to liquidate unliquidated IEEPA entries and to reliquidate non-final liquidations without regard to IEEPA duties, and he treated Learning Resources Inc. as a benefit for all importers of record.

- Administrative correction and reliquidation for unliquidated entries: This is typically the cleanest path because CBP can remove the invalid duty line before final liquidation and repay the excess deposit through normal processes.

- Protests for liquidated entries, where deadlines and finality rules dominate: Protest timing and scope are governed by statute and can become outcome-determinative, regardless of how strong the merits feel after the Supreme Court ruling.

- Credits, offsets, and negotiated settlements: Credits against future duty liability may be politically tempting, but they are a poor fit for importers that have changed sourcing or volumes, and they do not solve importer-of-record misalignment.

The Importer of Record Problem Is Not a Footnote

Refund entitlement generally follows the importer of record, not the party that bore the economic incidence. This divergence will drive the second wave of disputes. Under DDP and similar structures, a foreign seller may be the importer of record (IOR). In other cases, a U.S. subsidiary, nominee, or logistics intermediary served as importer of record for operational reasons.

The implication is straightforward: a firm can be economically out-of-pocket and still not be the party positioned to receive a refund. Where contracts are silent on refund allocation, expect disputes that are factual, document-heavy, and slow.

What Importers Should Do Now

The winning posture is administrative discipline. Treat the refund cycle as a documentation contest with deadlines.

- Build an entry-level inventory. Pull ACE reports identifying IEEPA duty lines, entry numbers, ports, brokers, duty amounts, and liquidation status.

- “Bucket” entries into unliquidated, recently liquidated, and older liquidated populations. Each bucket implies a different strategy and level of recoverability.

- Assemble complete entry packages. Assume CBP or counsel will want CBP Form 7501 data, proof of deposits, broker transmissions, and any correction or reconciliation history.

- Confirm who the importer of record actually is. Do not assume it aligns with who paid in commercial terms.

- Contract-map refund entitlement. Review tariff pass-through clauses, change-in-law language, and duty recovery provisions now, before the refund asset crystallizes.

Finally, keep an eye on litigation posture and the emerging market in refund rights. A large number of importers are already filing at the CIT to preserve claims, and a secondary market for refund rights has accelerated since the decision.

A Sober Outlook

The strongest reason to be optimistic is that the mechanics exist. If CBP reliquidates, §1505 provides a clear payment obligation, including interest, and a 30-day repayment clock.

Atmus Filtration is a reason for guarded confidence on mechanics for non-final entries, because it shows the CIT is prepared to give CBP a clear, administrable instruction set rather than leaving importers to litigate entry by entry.

The strongest reason to be cautious is that the Supreme Court did not dictate a refund remedy. That gives the government room to argue for narrower relief and forces the CIT to design a refund architecture that respects finality while giving practical effect to the holding.

For firms with meaningful exposure, the best strategy is to behave as if refunds are recoverable, but only after you prove entitlement with entry-level precision and fit within the remedial rules that will now emerge.

/Passle/6878183c1547331efeed13be/SearchServiceImages/2026-07-17-14-10-50-106-6a5a37eaa543841e34e7b987.jpg)

/Passle/6878183c1547331efeed13be/SearchServiceImages/2026-07-16-13-49-44-192-6a58e178c8545c9178cd5642.jpg)

/Passle/6878183c1547331efeed13be/SearchServiceImages/2026-07-15-13-39-17-604-6a578d855b77ac71bbc79e58.jpg)